Dissecting the intersection of

Economics, Geopolitics & Financial Markets

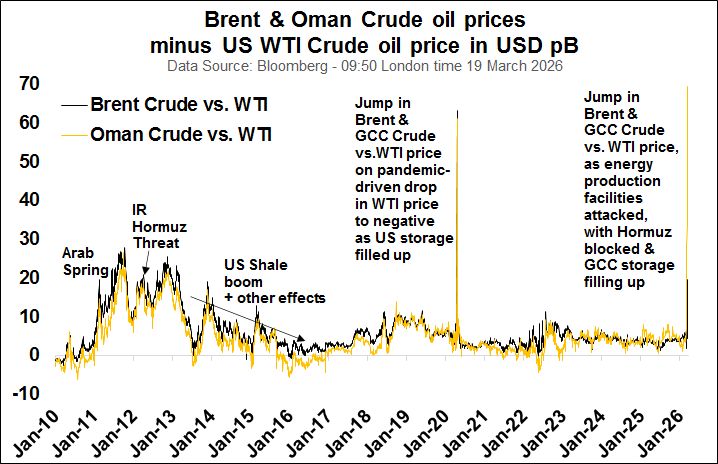

The last straw? Reciprocal attacks on energy facilities & questions on any US oil export restrictions has led to a huge jump in spread of Brent & GCC vs. US WTI oil prices. Last time was when the 2020 pandemic sent WTI prices plunging to negative territory as US storage filled up.

What next?

-Huge reactions like this usually see corresponding counter-actions (diplomacy?)

-As Brent & Oman vs WTI spreads show, global oil is currently not one market

-Are Saudi & UAE oil pipeline alternatives to Hormuz + IR flows now vulnerable too?

-That would leave only 3.3mn BpD IEA + 0.7 non-GCC OPEC&KAZ + China alternatives

-In extremis, the Hormuz deficit would thus rise to 15-16mn BpD or 14-15% of world output

-Avg. history estimates wd. then show Brent up 60% vs. 27 Feb levels or $116pB seen in morning of 19 March

-But as Brent vs. WTI spread shows, spikes can happen

-World has 7,800mn barrels in Crude + Oil products in storage (ex the IEA 400mn release), using IEA estimate

-China has 1,200-1,300mn barrels of oil in storage according to some estimates

-Will net oil importers be left to rely on their own storage?

-This is where regional cooperation (e.g. UK+EU) is vital

-Europe & Asia need to boost alternative energy solutions further

Please Note: All data/estimates are very rough and "ceteris paribus", given the fast-moving markets/news