Dissecting the intersection of

Economics, Geopolitics & Financial Markets

Hormuz & Oil: Price jump on alternative supply risks? On 18 March, Brent prices jumped above the $101pB avg. of the prior 7 days. Bloomberg economists looked at past crises/studies & concluded: oil prices rise by 4% on avg. for each 1% (=1.06mn BpD) drop in global supply. On 18 March, Brent was 50% higher than the $72.5pB on 27 Feb, indicating markets perceive a drop of around 13mn BpD in global Crude+Derivs supply (=50 ÷ 4 x 1.06).

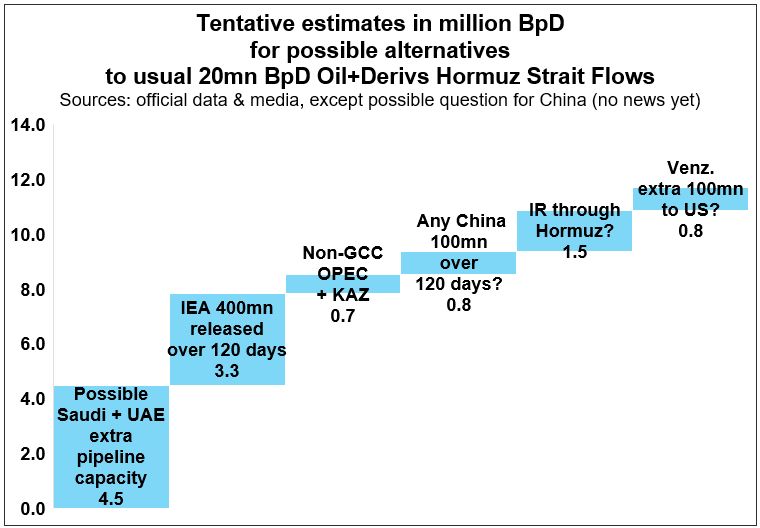

The chart below again highlights possible alternatives to the Hormuz 20mn BpD Crude+Derivs flows: a total 9.3mn BpD = 4.5mn (Saudi+UAE pipeline spare capacity) + 3.3mn (IEA emergency stockpile release over say 120 days ) + 0.7mn (possible non-GCC OPEC&Kazakhstan spare capacity) + 0.8mn (possible China emergency release). In addition, IR apparently still exports 1.5mn BpD through Hormuz, bringing possible total “alternatives” to 9.3+1.5=10.8mn BpD.

That leaves a Hormuz shortfall of 20 - 10.8 = 9.2mn BpD, which is 4mn less than the 13mn shortfall being priced by markets on 18 March (see above). Possible reasons for the latest price increase: Perhaps markets see upcoming risks re: 1) continued IR supply (Kharg Island), 2) Saudi & UAE pipeline vulnerabilities and/or 3) extra OPEC supply…