Dissecting the intersection of

Economics, Geopolitics & Financial Markets

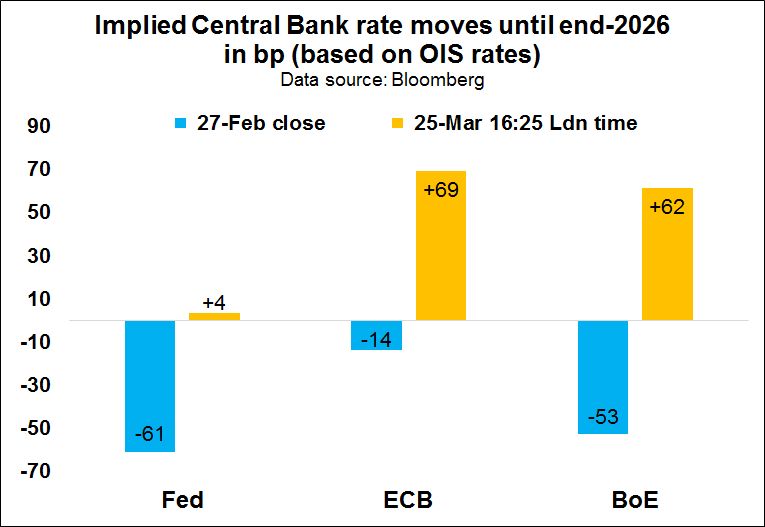

Markets have done much of the ECB, Fed & BoE work, with a fast turnaround in implied rate action. The whiplash has been strongest for BoE & ECB rates. The 2022 experience, when European CPI rose more & lingered for longer than the US, remains in everyone's memory. Ultimately, it is all a function of when & how much of the usual 20mn BpD Oil+Derivs (and LNG, Urea etc) flows through the Strait of Hormuz again. Current alternatives (incl. IR oil) are possibly around 11mn BpD Crude, which appears to be priced by oil markets. If Hormuz opens fully soon, a lot of the energy market chaos will be undone, providing way less arguments for central banks to hike rates...