Dissecting the intersection of

Economics, Geopolitics & Financial Markets

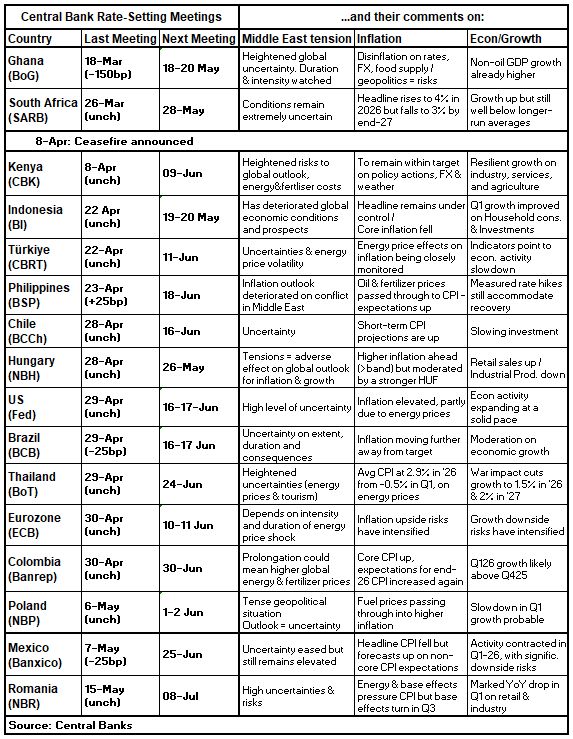

As inflation rises, EM central banks face the same Hormuz exogenous spillover risks. This CB meetings table provides a chronological path of their stepwise thought process. So far, that has been “wait-and-see”. The next step is action. A few observations:

1) SARB (26 Mar) possibly sums it up best: “The standard response to a supply shock is to look through first-round effects, which are unavoidable and cannot be stopped by interest rate changes. At the same time, central banks should be alert to second-round effects….Getting policy right means ensuring that the price response to supply shocks is transitory, and not persistent.”

2) “Uncertainty” is a word used by most, with some going further: SARB says “extremely uncertain”, BI (22 Apr) talks of “deteriorated global economic conditions”, the Fed (29 Apr) says “high level of uncertainty”. Note: the latter two were after the 8 Apr ceasefire.

3) Banxico (7 May) is the first in this list to say that “uncertainty…eased” (with the caveat that it “remains elevated”), while NBP (6 May) mentions the “tense geopolitical situation” and NBR (15 May) still talks of “high uncertainties”.

4) Philippines inflation has jumped the most thus far, with BSP (23 Apr) stating specifically that the “inflation outlook has deteriorated amid the ongoing conflict in the Middle East”. BSP is the first in this list to hike due to the jump in oil & fertiliser prices, neutralising its 25bp cut in February.

5) Besides BSP, CBK (8 Apr) and Banrep (30 Apr) have mentioned the risk from higher fertiliser prices. That list is likely to expand in countries where food has a larger weight in CPI baskets (Africa + some in Asia & Latam).

6) A mixed Econ/Growth picture, with BoG, CBK, BI and the Fed still talking about higher/solid/resilient growth. SARB, CBRT, BCCh, BCB, Banxico and NBR talk about already slower economic activity, but mainly on idiosyncracies.

7) Some CBs already mention forecast adjustments due to Hormuz spillover, including SARB (4% CPI in ’26, falling again to 3% in ’27) and BoT (Avg CPI up to 2.9% & growth down to 1.5% in ’26).

What next for EM if Hormuz remains closed? As SARB states, CBs need to ensure that “price response to supply shocks is transitory”. That means: signalling by CBs, closely followed by rate action, which is also very much a function of Fed action.